Authors: Mirco De Vincenzi, Elisa Donegatti, Ester Venturelli

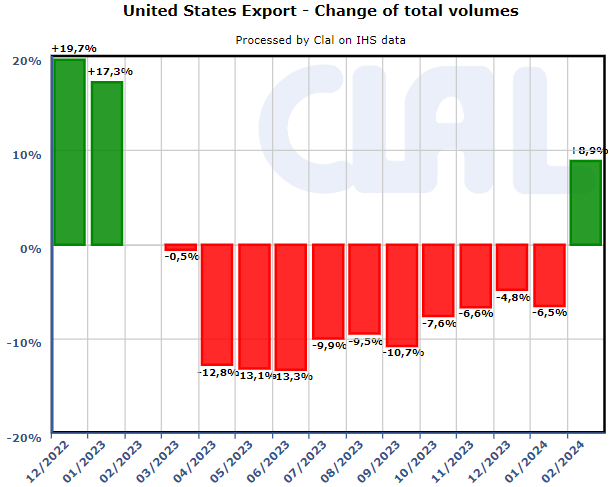

Clal.it – Monthly variations of exported quantities of dairy products from the US

For US dairy exports, February 2024 marked the first month with a positive change compared to the same month in 2023, after a year of negative variations. The recovery has been led by Cheeses that, overall, recorded an increase of +32,1% (+10.000 tons) associated with an average unit price of 4,56$/Kg, 15% lower compared to the price of a year before.

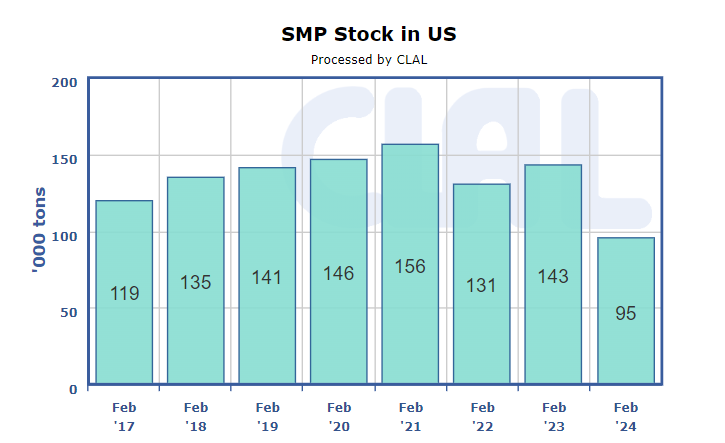

The lower prices also supported the exports of almost all the other major exported dairy products. Among those, the SMP (Skimmed Milk Powder) export recorded a decrease in flow towards Mexico that, however, has been largely compensated by a stronger demand from Asian countries. SMP production has been at minimum levels for several months which resulted in minimum stocks as well. This caused the downwarding trend of prices to stop and could result in an upward push if SMP demand increases.

Clal.it – US SMP Stocks

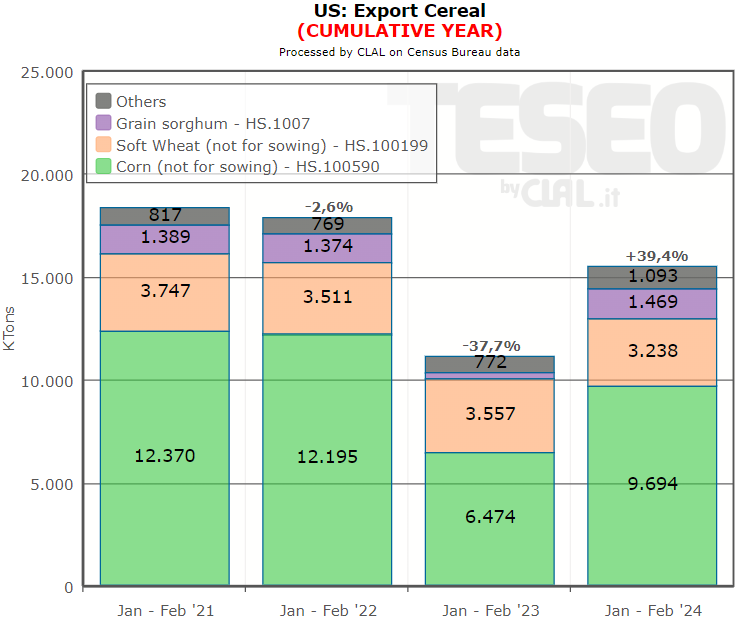

Concerning the agricultural sector, over the first two months of 2024 the Cereal export witnessed an overall increase of +39,4% compared to the same period of 2023, supported by the low prices that encouraged demand. Only Soft Wheat and Durum Wheat exported quantities were reduced, by -1,12% and -6,40%, respectively. The total increase of Oilseedsexport is +3,61%. Particularly, there has been an increase for Soybean Meal (+44,93%), due to lower quantities entering the market from Argentina.

The export of Hay and Alfalfa records a +21% increase in the first two months of 2024 compared to 2023, with the main destinations being Japan, China, and South Korea. However, these quantities are lower than those recorded in 2022, which had seen a record-breaking export.

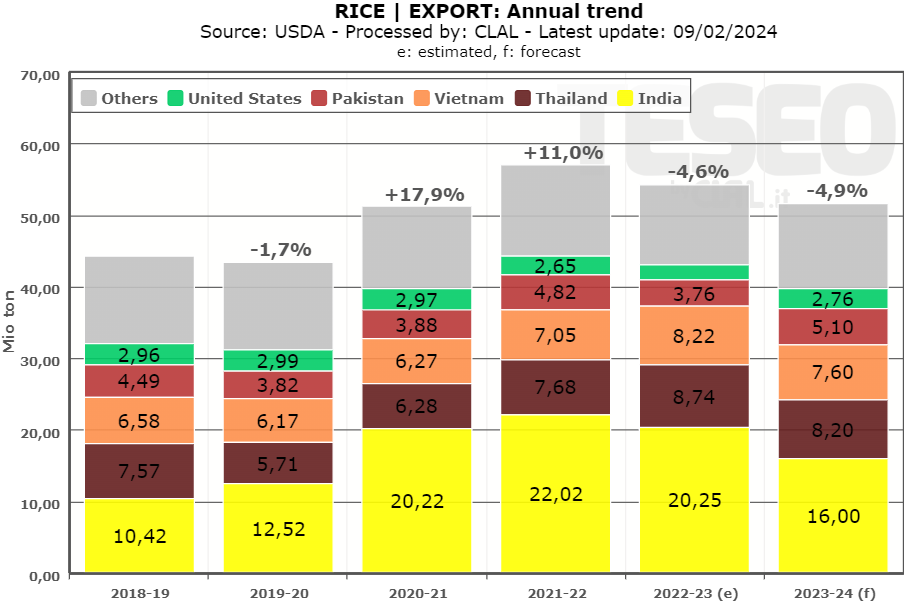

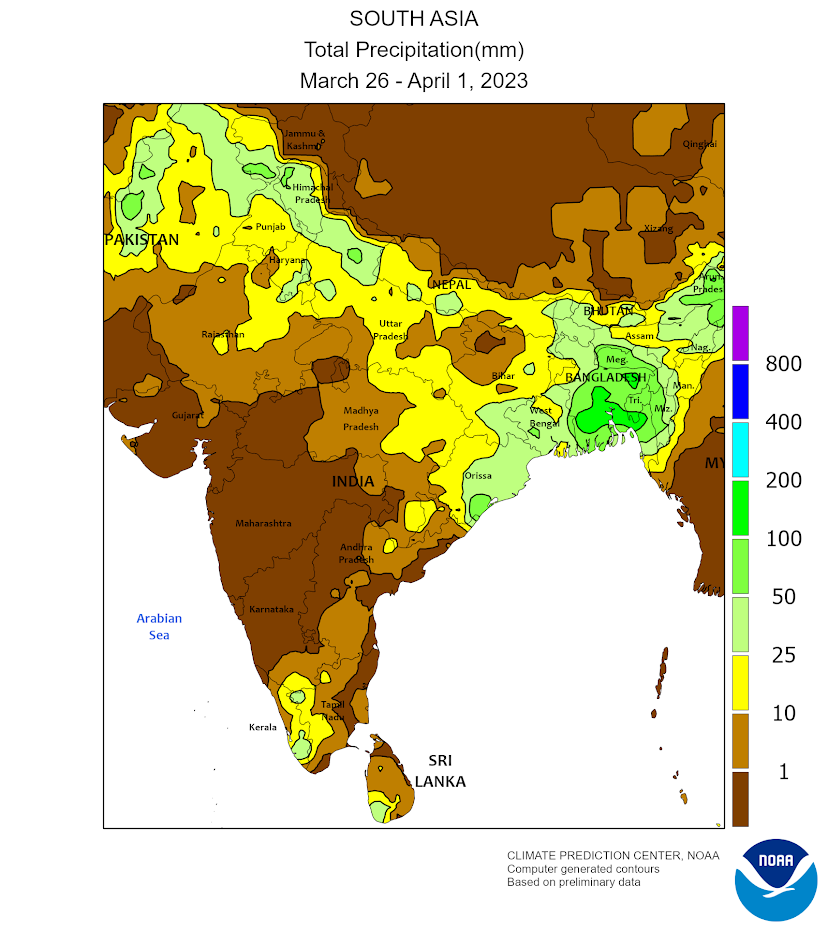

India is the second world producer of Rice, following China, with 132 Mio Ton in the 2023-24 season, according to USDA estimates. With a self-sufficiency of 112%, it is the first world Rice exporter with more than 20 Mio Ton in the 2022-23 season, about a 37% share of global Rice export.

In 2023, the Indian monsoon season has been characterised by little rain that damaged the main harvest of the country and, over the last months, the lack of humidity had a negative impact on the second harvest as well. Consequently, the Rice availability in the country is limited.

For that reason, last July the government forbade the export of white non basmati Rice, in an attempt to stop food price inflation, that last December was +10% compared to a year before. Moreover, a tax of 20% on the parboiled Rice export. Now, the government is considering the extension of that tax beyond the 31st of March, which is the current expiration date.

These tensions could have a bullish effect on the Rice markets, that are already recording prices at high levels in the Asian markets as well as the African and Middle Eastern markets

Corn and Soybean: the race between the US and Brazil

By: Ester Venturelli and Elisa Donegatti

For years Corn and Soy global export has been mainly led by two countries: the US and Brazil.

The perspectives of these two countries, however, are different: while the US are close to their maximum potential, in Brazil there is much more room for improvement for both cultivated areas and yields.

These developments are already going on in Brazil and are modifying the trade equilibria associated with the two products.

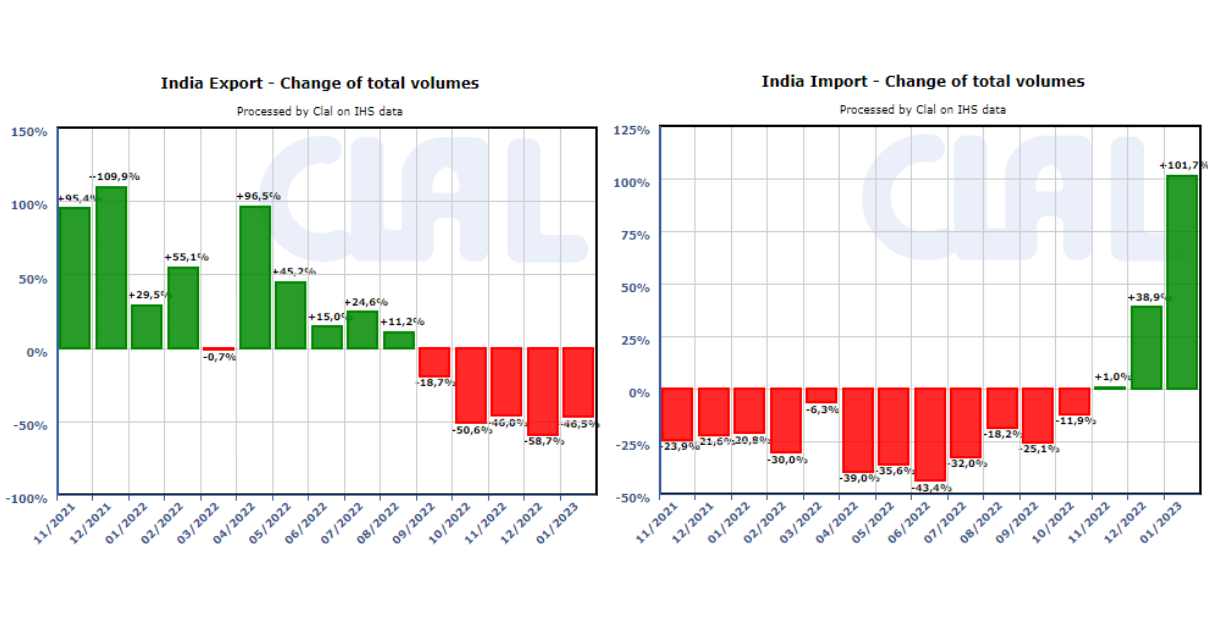

CLAL.it – India: Import and Export trends of dairy products

India is the main milk producer in the world. Nevertheless, domestic production is generally equal to consumption and the Country has a self-sufficiency of about 100%.

This year, though, we could observe dynamics that are very different from the ones to which we are used. Indian milk productions are influenced by several adverse factors that are causing a reduction of milk deliveries.

During the Coronavirus pandemic, dairy demand in India stopped, leading to a price drop. This led local farmers to limit the dimension of their herd. Since then, the recovery of productions has been slow also due to the rising costs of inputs following the post-Covid demand recovery and the war between Russia and Ukraine.

But that is not the only problem.

During 2022, the Country has been hit by an epidemic of Lumpy Skin Disease that, according to the estimates, has infected more than 300.000 heads. Even though the disease is not contagious for humans, its socio-economic impact is significant. Infected cattle show fever and skin lesions together with other complications that weaken the animal. Although the mortality associated with the disease is low, the recovery is rather slow. Indian milk productions have been significantly reduced.

Moreover, in the last months, India was hit by heat waves that damaged harvests, reducing wheat and fodder availability.

In this context of slowed production, demand, after recovering from the stop due to Covid, has increased. The result of the disequilibrium between offer and demand has been a significant rise of retail prices.

Domestic market tensions opened the doors to international markets and the Country’s dairy imports already recorded important increases. The Government is evaluating the removal of import taxes on dairy products to alleviate the market tensions.

CLAL.Teseo.it – Precipitation trend in India (latest available week)

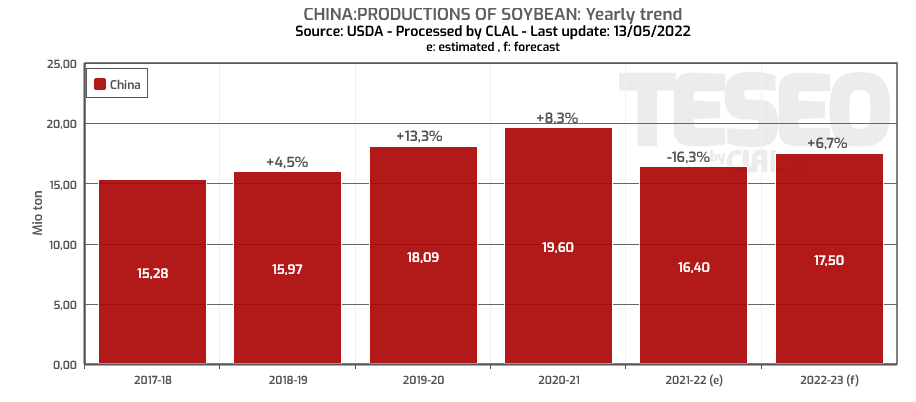

Rising Soybean local prices and production in China

With over 66 million tonnes of Cereals and over 102 million tonnes of Oilseeds imported in 2021, China is the largest importing country in the world. Furthermore, China holds 68% of the world Corn stocks, 36% of the Soybean stocks and nearly 51% of the world Wheat stocks.

With these volumes, it is very important to know the prices of Chinese agricultural products, the possible market trends, the value of commodities on the local market and in the main China’s suppliers, as well as the progress of sowing and cultivation estimates.

In 2022-23 season, for example, China is projected to increase domestic Soybean production compared to the previous campaign (+ 6.7%, source USDA), while is expected to reduce the production of Corn (-0.6%) and Wheat ( -1.4%). The expected production should amount to approximately 271 million tons of Corn, 17.5 million tons of Soybeans, 135 million tons of Wheat.

TESEO.clal.it – China: Soybean production

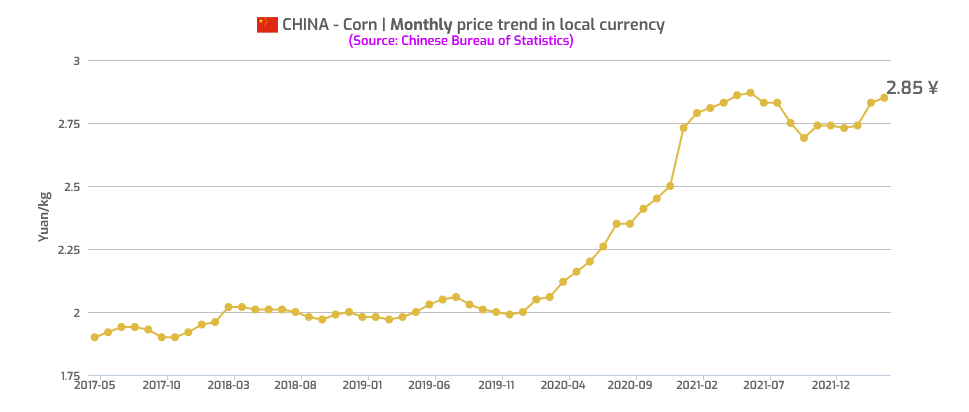

Also in April 2022 the increase in local prices of Corn, Soy and Wheat continued. Domestic prices are placed on values higher than import prices, probably due to political will to support domestic production of commodities.

TESEO.clal.it – China: Corn local prices

The new page of TESEO “China: prices of agricultural products” allows you to follow the prices and trends of Corn, Soy, Wheat and even Tomato, which sees China as the largest Producer worldwide. This information, together with the seasonal forecasts of Chinese production, allow companies to partially plan their future actions, to contribute to having an increasingly reliable and complete internal balance sheet, bearing in mind, however, that elements of uncertainty can change prices, markets and plans.

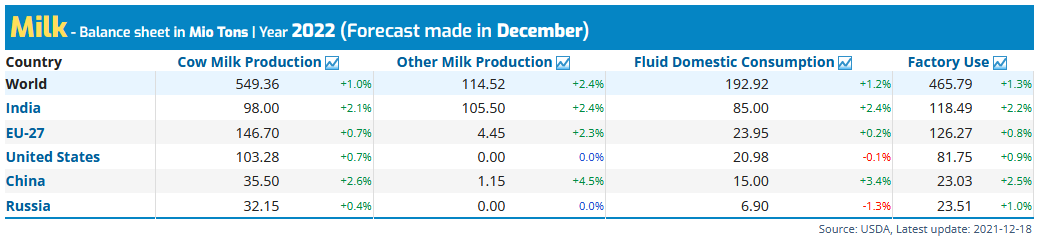

India plans to grow exports of dairy products (and not only)

With cow’s milk production expected to increase in 2022 (+2.1%) as well as other types of milk such as buffalo, sheep and goat’s milk (+ 2.4%, source USDA), India aims to export to Countries in SouthEast Asia and Middle East and Northern Africa.

CLAL.it – Milk Balance Sheet Season 2022

India is a subcontinent with an area almost 11 times larger than Italy, self-sufficient in the dairy sector (100.2%), with a per capita consumption of drinking milk which in 2021 rose to 54.1 liters per capita. Despite being one of the most populous countries in the world, with about 1.4 billion inhabitants, Indian agri-food exports amount to about 50 billion euros overall, about the same as Italy.

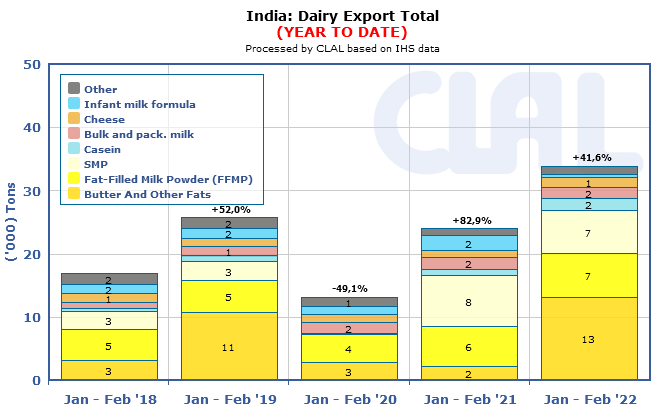

India’s ambition is to establish itself as an exporting country, in particular of Butter and other fats, mainly destined for the United Arab Emirates, Saudi Arabia, Indonesia, Oman, Bahrain, Morocco and Qatar, Fat Filled Milk Powder (FFMP), mainly exported to Bangladesh, Sri Lanka, Malaysia, UAE, but also US and UK, SMP, which mainly finds its way to Bangladesh.

Between January and February 2022 total exports of Indian dairy products grew by 41.6% compared to the same period of the previous year, which grew by 82.9% compared to January-February 2020, despite being a period held back by the spread of Covid, which claimed several victims in India.

For the first time, in 2022, Indian dairy exports exceeded 30,000 tons in the first two months of the year.

Overall, foreign sales of dairy products reached 150,000 tons in 2021.

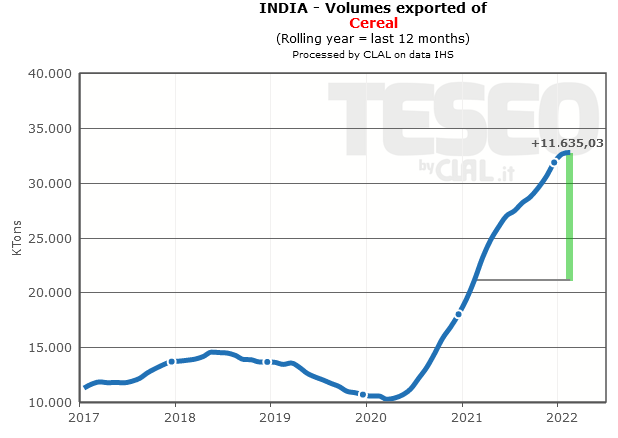

Thanks to the favorable climate season, cereal crops are encouraging exports, which have been consistently on positive tracks since the beginning of 2020.

The first two items of Indian cereal exports are Rice (+46% exports in 2021 compared to 2020) and Wheat (+ 453.1% exports in 2021 compared to the previous year), a trend that kept positive also over the first two months of 2022 (+2% the export of rice in quantity and + 123% the export of wheat, the latter with an even more impressive boom in value: + 162.7%).

Among the main countries of destination for rice we find China, Nepal, Iran, Benin, Ivory Coast and Sri Lanka, while the Indian wheat trade routes are Bangladesh (with a market share of 50%), Sri Lanka, Indonesia, South Korea and Philippines.

The agrarian reform, strongly contested by farmers, was filed last November as India aims, on the one hand, to strengthen the technologies for agriculture development and the spreading of solutions for agri-food products’ conservation. On the other hand, the Country aims to accelerate infrastructural growth, a key element for the transport of foodstuffs both within India and abroad.

It’s always the same story: a barn to rebuild, struggles finding workers, not enough land to reliably grow forage and other crops… the dairy is shutting down. It is a sad story, common to more and more places where dairy industry has to face the challenges of the market. However, when it happens to a family farm with 150 cows that started dairying in 1935 and was the oldest local source for homogenized milk, the loss is great.

It’s hard to produce milk in Alaska, with long and severe winters, poor soils and the problem of competing with cartons of imported milk. Dairing was a widespread activity at the beginning of the last century and attracted farmers from Europe such as the Havemeister family who arrived from Germany in the 1920s. Dairies in Alaska began struggling decades ago despite state subsidies.

What was economically viable until a few decades ago is now outdated, obsolete, unprofitable. To run a farm is a hard job but it ensures the protection of the territory and it enhances the local productions. Livestock manure enriches the soil by releasing nutrients that improve its fertility and thus contributing to maintain biodiversity.

A story of people and animals

Any farming operation is not simply a business. It is an integral part of a community, first and foremost a story of people and animals.

The Havemeister family had to shut down their dairy in Alaska after 90 years of hard work through multiple generations. About ninety of the 150 cows will go to the slaughterhouse, the remaining to another dairy, among the few left open.

Local consumers will find milk in their trusted store produced and packaged far away. Nowadays the major reference is the price no matter where and how the product is obtained. Therefore either you are competitive or close. Forever.

Ester’s Opinion

Ester Venturelli – CLAL and TESEO Team

The closing of small farms certainly is a sad news, since it represents a loss of heritage, particularly from a cultural perspective. Even more, if the closing farm is among the few farms in a not particularly vocated area.

Unfortunately, the GDP has been the main indicator for countries’ development since the second post-war. This has led to a widespread mindset, extremely focused on productivity and profits, whose negative effects we see now. Nevertheless, these goals remain essential aspects of a farm, whose main aim is the financial support of the people working there.

The ideal would be a society that, more than quantity, appreciates quality and values a product according also to its collateral aspects (culture, environment, society). When consumers are unable to recognise this kind of added value, the government should undertake this role, not by adopting a dependence approach, but rather by giving a fair compensation for the resulting positive externalities. This would allow virtuous enterprises to keep operating in their area.

Ester Venturelli, Market Analysis and Agricultural Policies – CLAL and TESEO

Favorable weather for milk production in Oceania and South America [The Austral - August 2021]

The Austral news offers the latest information on the dairy market in Oceania and South America.

Oceania: active interest from Northern Asian and African Butter buyers

New Zealand+4.5%milk production

Jun-Jul 21 y-o-y

In New Zealand, milk production in July 2021 recorded +6.6% compared to July 2020. So far, the weather has been favorable for pasture growth and cow comfort. Farmers in Australia also have relatively good weather, reasonable input costs, and favorable opening milk prices.

New Zealand company Happy Cow Milk has built a platform that enables dairy farmers to supply ethical and sustainable milk to their local community, with the aim of reducing carbon emissions and plastic waste. This business has reached its $500,000 crowdfunding target.

In June 2021, WMP exports to New Zealand and Australia increased significantly, particularly in Southeast Asia.

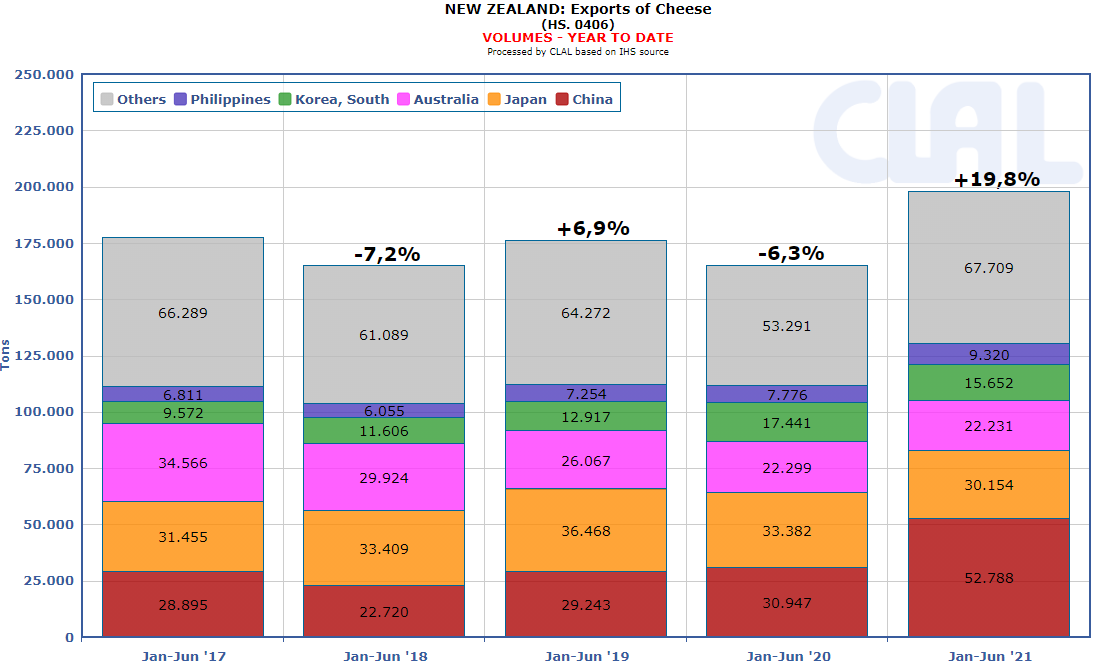

For New Zealand, the positive trend in Cheese exports is confirmed, which closes the first half of 2021 with 197,854 tons (+19.8% compared to the first half of 2020), mainly destined for China and other Asian countries.

As Delta variant COVID cases increase, New Zealand has reached its highest level of alert and outbreaks across Southeast Asia are creating other regional lockdowns. These new outbreaks and health safety measures may impede dairy demand and distribution.

Funding for expansion to Southeast Asia

The Australian government has awarded funding to the dairy industry to work to reduce technical trade barriers, such as product testing, shelf life and labeling. The government and industry stakeholders will work to expand opportunities in Southeast Asia with the funding.

Following four months of Global Dairy Trade price index declines, event 290 on August 17th has resulted in the GDT price index lifting, albeit by 0.3%. Northern Asian and African Butter buyers bought heavily at the event.

The average prices of dairy products in Oceania follow the trend of the latest GDT event, with increases for Butter, Cheddar and SMP, and a decrease for WMP, whose price remains above the levels of a year ago.

CLAL.it – New Zealand: Cheese Export

South America: pizzerias and restaurants are ordering additional cheese supplies

Spring-like climate conditions are lingering in the main dairy basins of Argentina and Uruguay. Despite some concerns about a possible rebound in feed prices, market participants report milk prices are good.

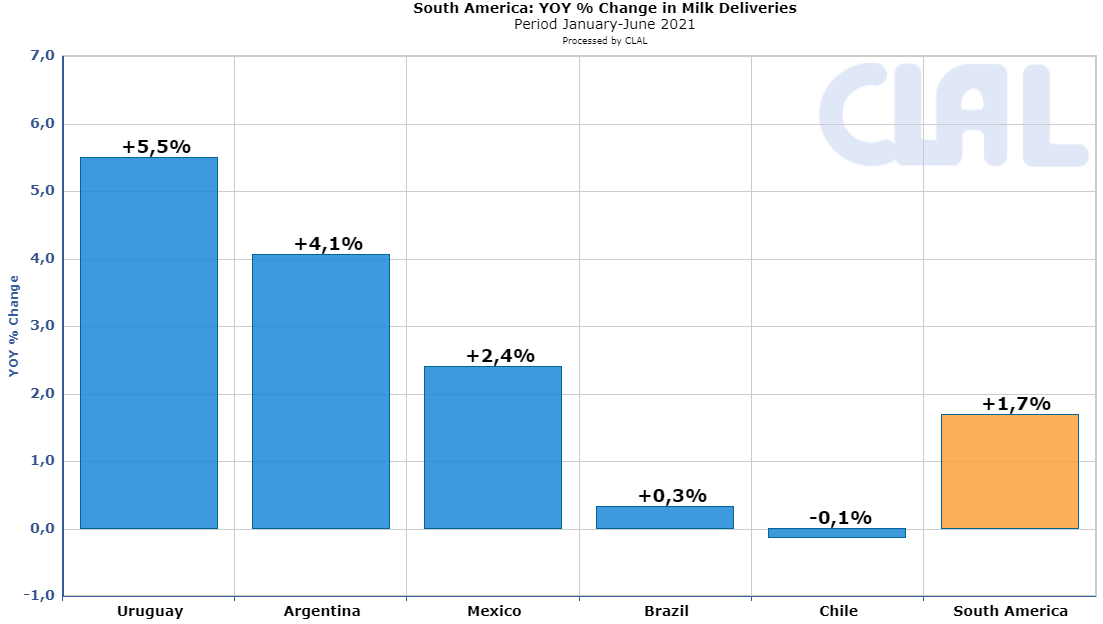

Milk deliveries in South American countries increased in the first half of 2021, with the exception of Chile, where the previous year’s production sprint seems to have stopped.

The prices of SMP and WMP reflect the trend of the main international markets, with SMP slightly increasing and WMP decreasing compared to the previous weeks.

The performance of the Cheese market was very positive, thanks to the additional supplies ordered from pizzerias and restaurants, and the increase in Argentine exports to other Latin American countries.

CLAL.it – South America: milk deliveries change in the first half of 2021

Source: CLAL processing on USDA, IHS and local sources.

Note: assessments about market trend are expressed in US$

The videonews “Agricultural Market” offers a selection of recent information on agricultural commodities used for livestock feeding.

Severe climatic events are affecting different parts of the world. California,Canada and Brazil are experiencing extreme drought.

The heat wave also hit the Scandinavian countries.

On the contrary, heavy rains hit Western Europe hard, especially Germany.

A few days ago, floods also occurred in China.

The effects of these climatic phenomena have not yet been estimated, but they could affect agricultural production around the world.

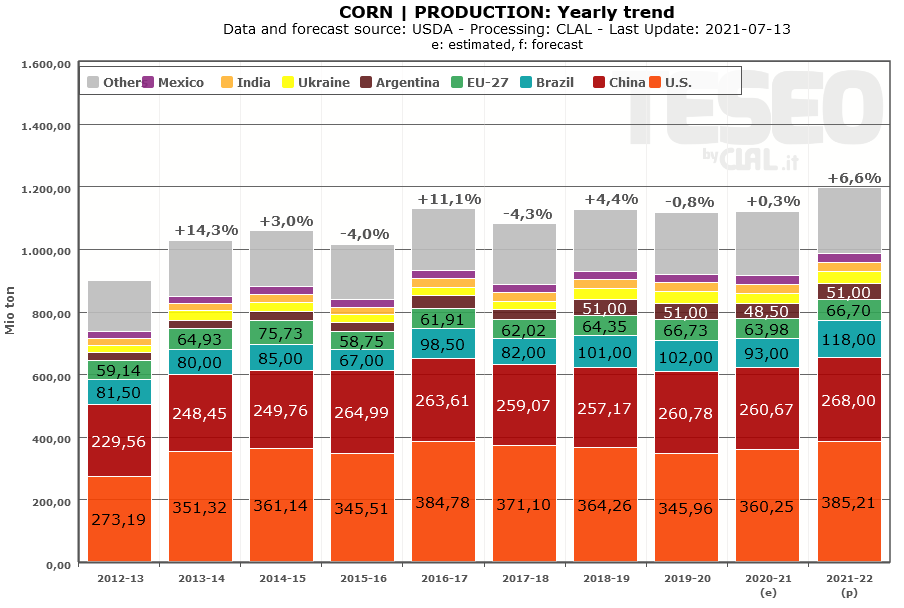

CORN

For the new season, which will start on September 1, production is expected to increase for the main countries compared to the previous season, after the difficulties encountered in the 2020-21 season, including the current drought in Brazil.

Chinese imports are expected to be stable, despite the policy of reducing the use of corn in animal feed, aimed at supporting the use of alternative raw materials.

Trade Update – European corn imports in the first 5 months of 2021 were lower than last year, reflecting a sharp decline from Ukraine. Italy’s imports recorded a decline in April.

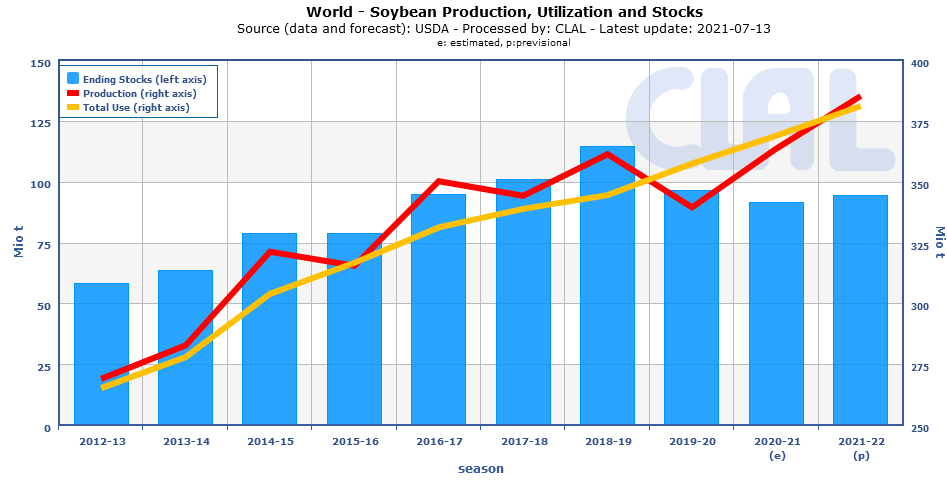

SOY

Global soybean trade has slowed in recent weeks. With Chinese demand as the driving factor, the weakening export pace can be attributed to a softening of Chinese purchases. Soybean stocks in China, already at high levels, continue to grow as earlier imports exceeded the monthly crush pace.

Soybean availability in the United States is expected to increase, but exports could suffer from competition with South America, where larger availability is expected for the October-December period.

Trade Update – EU-27 Soybean imports in May 2021 decreased significantly, especially from Brazil and Canada. Italy follows an opposite trend, in fact it imported significant volumes from Brazil, but Canada and the United States do not appear among the main suppliers in May.

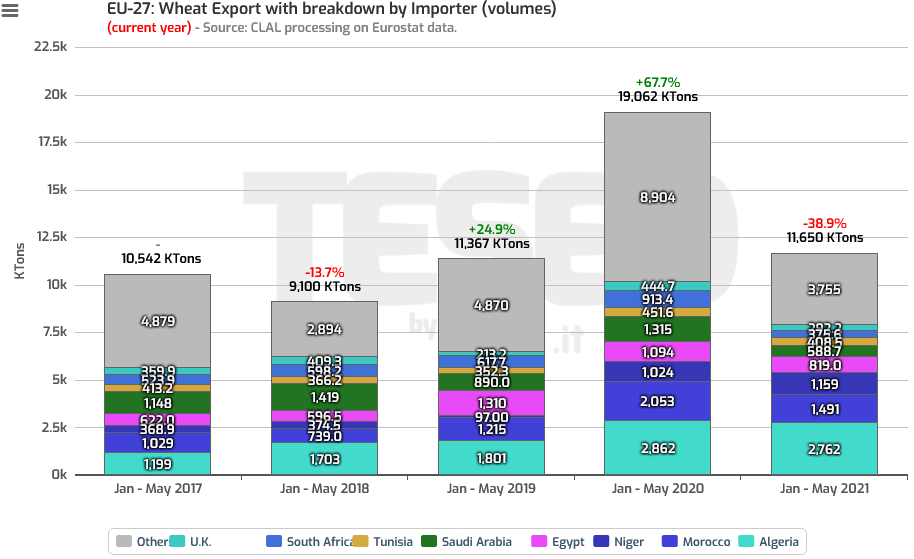

WHEAT

High yields in the EU-27 have led to an increase in supply. After the low temperatures and droughts in April and May, the wheat harvest benefited from a more favorable climate.

All North African countries have implemented domestic support policies that encourage domestic wheat production and seek to lower dependency on international suppliers. This could affect the export of the EU, the main supplier, which competes with Russia, Ukraine and Canada on this market.

Australia is a new competitor in the Asian markets for Canada and the United States. The production and exports of the two North American countries are expected to decline, also as a result of the changed use of agricultural areas for other crops. The lower availability could support the high export prices.

Trade update – EU-27 total Wheat exports in the first 5 months of 2021 were lower than last year, however Durum Wheat exports to Tunisia recovered in May 2021. In the first four months of 2021, Italy exported 66,555 tons of durum wheat to Tunisia and Algeria.

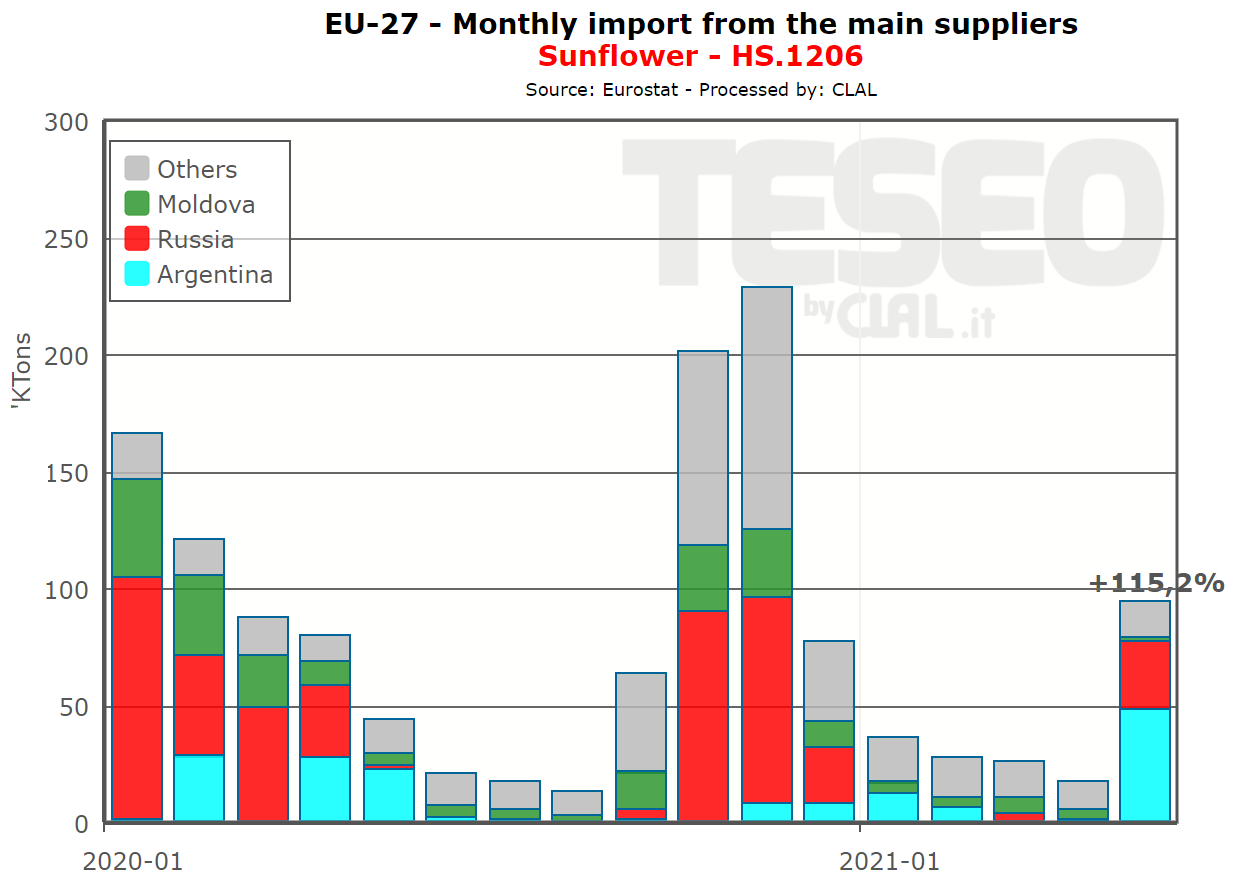

SUNFLOWER SEEDS

Sunflower Seed production in Russia is estimated at record highs for the new season, with crop areas and yields on the rise.

In Italy, the cost of proteins obtained from whole grain Sunflower extraction meal is, from April 2021, higher than that of proteins obtained from Soybean extraction meal.

Trade Update – After a few months of decline, European Sunflower seed imports recovered in May 2021, with significant increases from Argentina and Russia.

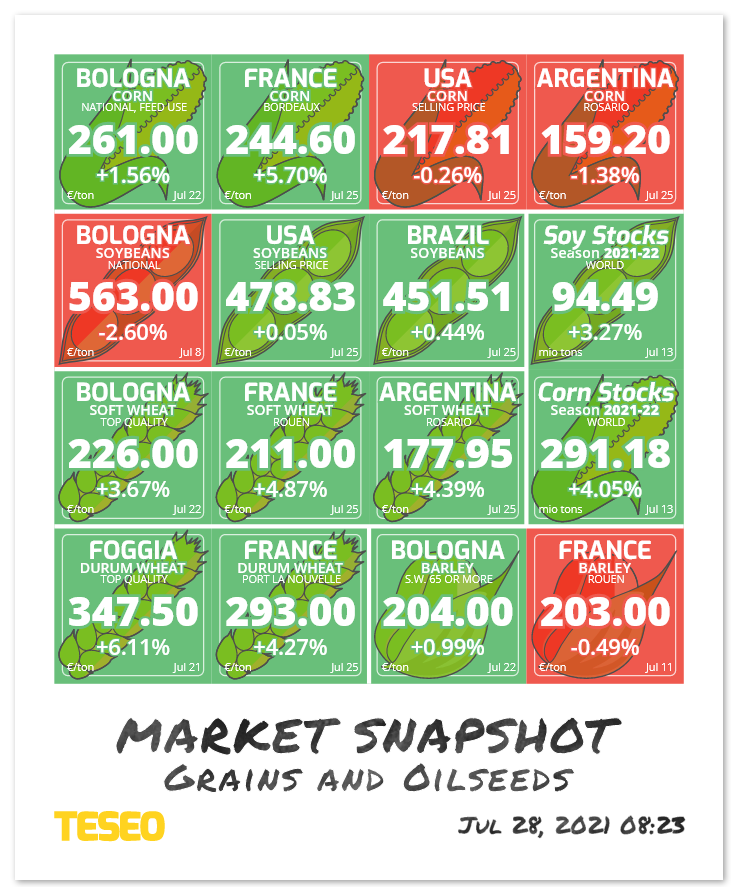

Market Snapshot

This infographic shows some key variables to analyze the situation of the Italian and international market at a glance.

The colors represent the variation: red for a decrease, green for an increase, blue for stable values, gray with an orange background for unquoted values.

The new production season for Oceania has begun [The Austral - July 2021]

The Austral news offers the latest information on the dairy market in Oceania and South America.

Oceania: agreement to phase out tariffs on dairy exports between Australia and United Kingdom

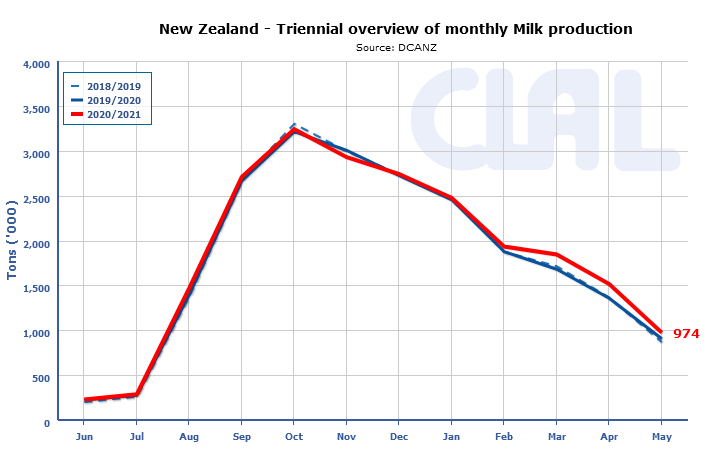

Most dairy producers have dried off most cows

With an increase of +7.6% in May 2021, the dairy season in New Zealand ended with +2.6% on a tonnage basis. New Zealand sources believe that supplemental feeding helped to boost New Zealand milk production in the season just ended.

On June 1st, the new season began and at this time of year most dairy producers have dried off most cows.

There is concern about the labor shortages due to the likelihood that migrant dairy workers will not be able to come into New Zealand to work for a number of months due to COVID-19 related travel restrictions.

CLAL.it – New Zealand milk production

Milk production in Australia recorded +2.6% in May 2021 and the overall trend of the first 11 months of the 2020-21 season reports an increase by +0.8%.

July 1 marked the opening of the new milk season in Australia. During the last few weeks leading into the new season something of a “bidding war” broke out. Major processors began lifting offering prices to be sure they have enough milk geographically located for dairy manufacturing plants they operate. As a country with a huge land area and climatic variety, prices offered in varied regions do differ from other regions.

The prime ministers of Australia and the United Kingdom reached an agreement in principle affecting dairy trade. Upon ratification, tariffs on Australian dairy exports to the UK will be eliminated over five years.

Following the announcement of this agreement, many dairy firms in New Zealand are pressuring officials there to secure a similar deal. There seems to be general agreement in New Zealand to pursue this course of action, however, dairy officials anticipate there is not likely to be an identical deal as was reached with Australia.

In May 2021, the export of dairy products increased both for New Zealand (+21.1%) and for Australia (+47.3%). China is the main destination for New Zealand’s WMP, Drinking Milk and Cheese, and for Australia’s WMP and SMP.

Dairy prices range widened

Average dairy prices in Oceania decreased and the price range widened. The lower range dip reflects the last GDT event of 6 July 2021 and the upper range prices reflect the interest of Asian buyers. Only the SMP showed a slowdown even in the upper range price, reflecting supply that has grown beyond demand.

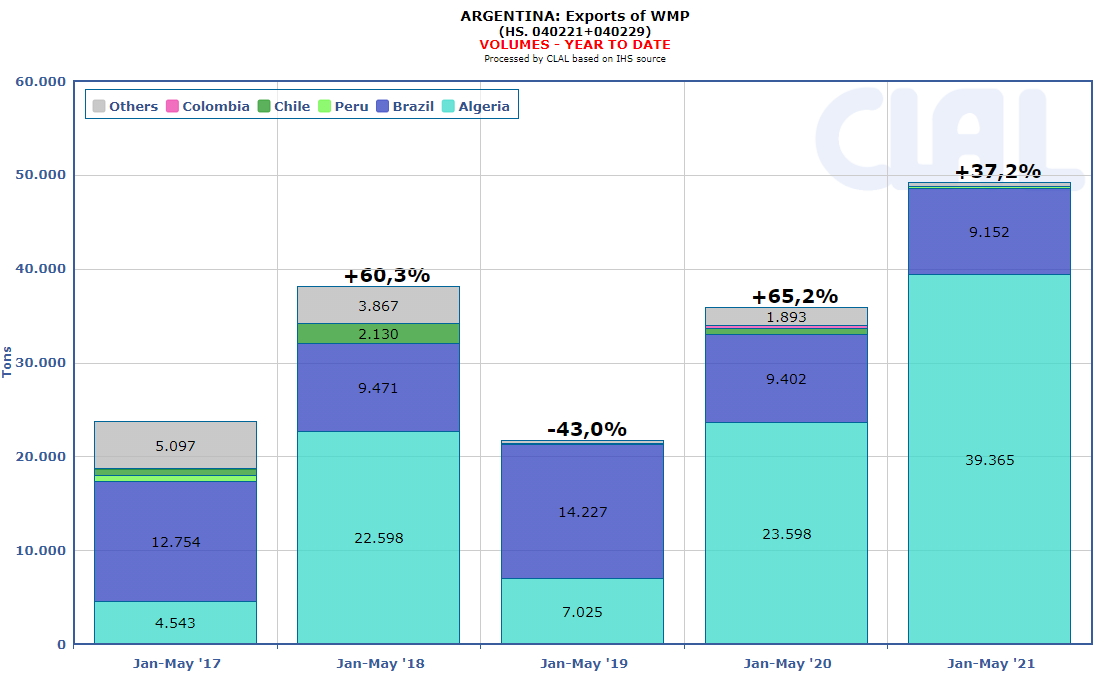

South America: Argentina is the first WMP supplier for Algeria

Milk supply also increased in May 2021 in Argentina and Uruguay, by +3.4% and +6.2% respectively. The current production is meeting most production needs from dairy processors.

Cheese and Yogurt sales decrease seasonally. The priority destination in several processing plants is UHT milk.

SMP and WMP stock levels are increasing and their prices reflect the downward movement of the main international markets.

In 2021, Argentina is becoming Algeria’s main WMP supplier country. In the period January-May 2021, Argentina’s WMP exports to Algeria amounted to 39,365 tons (+66.8% compared to the same period in 2020).

CLAL.it – Argentina: WMP Export

Source: CLAL processing on USDA, IHS and local sources.

Note: assessments about market trend are expressed in US$

For the new season, which will start on September 1, production is expected to increase for the main countries compared to the previous season, after the difficulties encountered in the 2020-21 season, including the current drought in Brazil.

For the new season, which will start on September 1, production is expected to increase for the main countries compared to the previous season, after the difficulties encountered in the 2020-21 season, including the current drought in Brazil.

Global soybean trade has slowed in recent weeks. With Chinese demand as the driving factor, the weakening export pace can be attributed to a softening of Chinese purchases. Soybean stocks in China, already at high levels, continue to grow as earlier imports exceeded the monthly crush pace.

Global soybean trade has slowed in recent weeks. With Chinese demand as the driving factor, the weakening export pace can be attributed to a softening of Chinese purchases. Soybean stocks in China, already at high levels, continue to grow as earlier imports exceeded the monthly crush pace.

High yields in the EU-27 have led to an increase in supply. After the low temperatures and droughts in April and May, the wheat harvest benefited from a more favorable climate.

High yields in the EU-27 have led to an increase in supply. After the low temperatures and droughts in April and May, the wheat harvest benefited from a more favorable climate.

Sunflower Seed production in Russia is estimated at record highs for the new season, with crop areas and yields on the rise.

Sunflower Seed production in Russia is estimated at record highs for the new season, with crop areas and yields on the rise.