Period: March 6 – 17 , 2017

AUSTRALIA

- Milk production: in January was -5.9% below January 2016.

NEW ZEALAND

- Weather situation: the autumn has been good. Increasingly this is considered a sign that could lead to higher milk production than previously expected.

MILK PRODUCTION

- Australia *: -8.21% (Jul 16 – Jan 17 vs. Jul 15 – Jan 16)

- New Zealand *: -2.61% (Jun 16 – Jan 17 vs. Jun 15 – Jan 16)

BUTTER (82%): prices strengthened at the bottom of the price range: greater anxiety over tighter dairy fats supplies is sustaining this market.

CHEDDAR CHEESE: prices weakened. Some customers have been increasingly feeling that prices have run up a bit too quickly and are comfortable with a price correction.

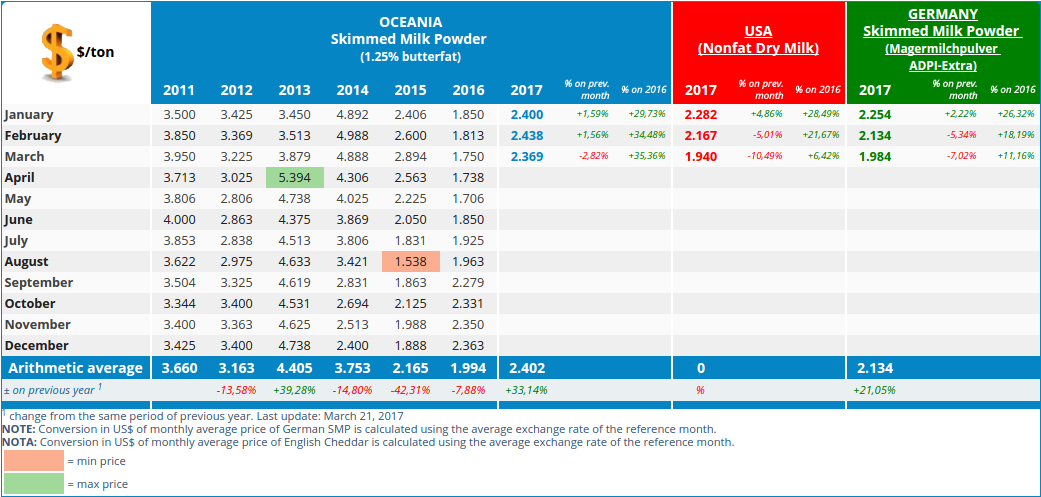

SMP: prices significantly declined, narrowing the differential with European SMP prices. There was increasing resistance to Oceania SMP pricing from some buyers who found European pricing attractive. Moreover, increasing belief in milk production higher than estimated made some buyers wary of recent pricing levels.

WMP: prices weakened significantly, reflecting March 7, 2017 GDT event outcomes. This reverses the previous situation where Oceania WMP pricing was a bit higher than in Europe.

The weakness in a number of March 7, 2017 GDT event results could be attributed to several factors:

- some observers believe excessive volumes of some products were offered;

- sentiment that some recent pricing has been a bit too high above market transactions;

- lingering suspicion that New Zealand milk production will be higher than projected.

CLAL.it – SMP prices in Oceania, United States and Germany

Note: · Assessments about market trend are expressed in US$; · * Dairy season: July, 1st – June, 30th (Australia), June, 1st – May, 31st (New Zealand).

Source: USDA summarized by the CLAL Team

More informations about milk production in New Zealand and Australia are available on CLAL.it

... share

... shareThe CLAL.it team is composed of young people who with the help of Computer Science study the dairy market and develop tools to provide the Operators of the dairy sector with a comprehensive real-time view of the national and international market trends.

Leave a Reply

You must be registered and logged in to post a comment.