New Zealand: dairy market remains bearish [News Oceania n°14/2015]

Period: June 29 – July 10, 2015

AUSTRALIA

- Milk production: season concluded at the end of June. Milk production for the season was above the previous year with estimates of a 2-3% increase. May 2015 milk production was 1.15% above May 2014.

- Milk producers: hay market has a firm undertone. Stocks are seasonally low and rainfall over much of the dairy producing region has been below average.

NEW ZEALAND

- Milk production: is at seasonally low levels. Most dairy cows are dried off and on winter pastures. Milk production season concluded at the end of May. Milk production for the season was up 2.84% from the previous year. May milk production was up 10.7% from May 2014. Calving will begin in another week or so and milk production will start to increase.

- Weather situation: cold temperatures are forecasted for the coming week, with rain or snow in most areas of the country.

- Milk producers: pastures and forages are in normal to good condition for this time of year.

MILK PRODUCTION

- Australia *: +2,79% (Jul 14-May 15 vs. Jul 13-May 14)

- New Zealand *: +2.84% (Jun 14-May 15 vs. Jun 13-May 14)

BUTTER (82%): prices decreased, trading is light. New Zealand has stocks available, while supplies for export in Australia are tight. Demand is seen as steady with increased interest coming from the Middle East and North Africa. The end of Ramadan (July 17) may provide an additional boost to demand.

CHEDDAR CHEESE: prices moved lower. Discounts on spot sales as some manufacturers attempted to lower inventory levels prior to the end of their fiscal year. The return on cheese appears significantly above the return for milk powders and thus increased milk flows to cheese vats are expected in the coming season. European competition increased on Q4 contracts. Demand is fairly steady with good interest coming from Asia.

SMP: prices moved lower. Supplies are more readily available in New Zealand than Australia. Existing supplies and increasing production in the coming weeks are contributing to the market’s weak undertone. Demand is light. Some buyers are negotiating for a fixed price through 2016.

WMP: prices moved significantly lower. New Zealand manufacturers are attempting to lower current supply levels prior to the close of their financial year (end of July). Demand is very sluggish with limited interest from China. Large volume buyers are purchasing hand to mouth. The impending start of the new production season contributes to the very weak undertone in the market.

New Zealand dairy manufacturers are attempting to reduce their remaining stocks of dairy commodities by the end of July with mixed results. Demand is sluggish as many buyers have more than adequate supplies. Numerous market analysts expect the “bearish” market conditions to continue through 2015 and into 2016.

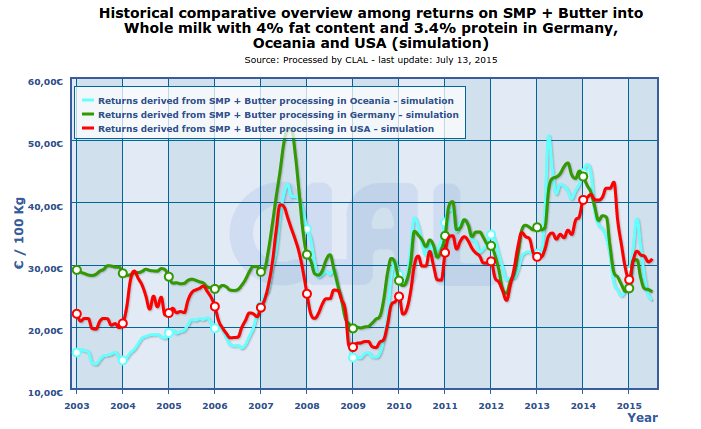

CLAL.it – Oceania, Germany and US: returns on SMP + Butter

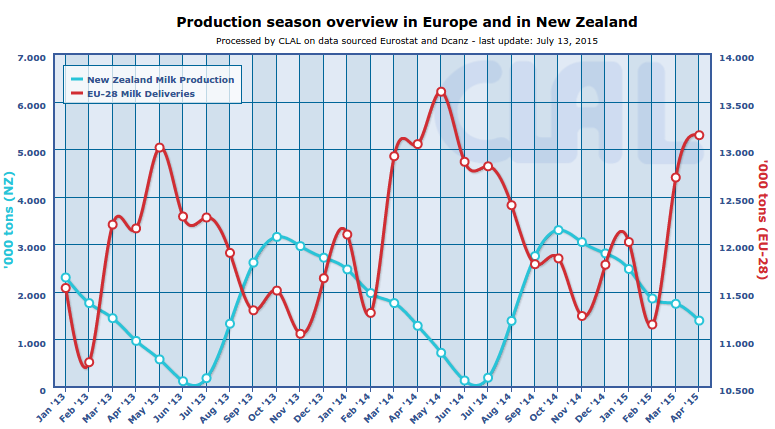

CLAL.it – Milk production seasons in New Zealand and Europe

Note: · Assessments about market trend are expressed in US$; · * Dairy season: July, 1st – June, 30th (Australia), June, 1st – May, 31st (New Zealand).

Source: USDA summarized by the CLAL Team

More informations about milk production in New Zealand and Australia are available on CLAL.it

The CLAL.it team is composed of young people who with the help of Computer Science study the dairy market and develop tools to provide the Operators of the dairy sector with a comprehensive real-time view of the national and international market trends.

Leave a Reply

You must be registered and logged in to post a comment.