Fonterra revised its 2018/19 forecast Farmgate Milk Price [News Oceania n°21/2018]

Period: October 1 – 12, 2018

Australia

-3.6% milk production August 2018 y-o-y

Milk Producers, faced with higher prices for feed and less water availability, are reducing the herd sizes by 25% (the typical annual culling involved about 20% of herd sizes).

New Zealand continues to benefit from nearly ideal conditions for milk production, which in the first quarter of the 2018-19 production season is 5.5% higher than the same period of the previous season.

Fonterra increased its forecast New Zealand milk collection volumes by 1.3% to 1,550 million kgMS and revised its 2018/19 forecast Farmgate Milk Price from 6.75 NZD/kgMS to a range of 6.25-6.50 NZD/kgMS

Lower prices for the dairy products

This is especially true for WMP, which is the most important New Zealand dairy product exported in terms of dollar value. With exports remaining generally steady, some WMP plants are comfortable to slightly back off and let more milk flow to other uses, often Cheese and Butter plants. The lower prices have led to more recent interest from Buyers such as China in contracting for future deliveries.

Oceania Cheddar prices are slightly down. Production is increasing, made possible by increasing milk volumes now being available to cheese plants.

Buyers are contracting to lock in current Butter pricing

The SMP market is also down. It is still early in the season and there is plenty of SMP available for interested Buyers. Contracting is moving but not with any real sense of urgency among Buyers.

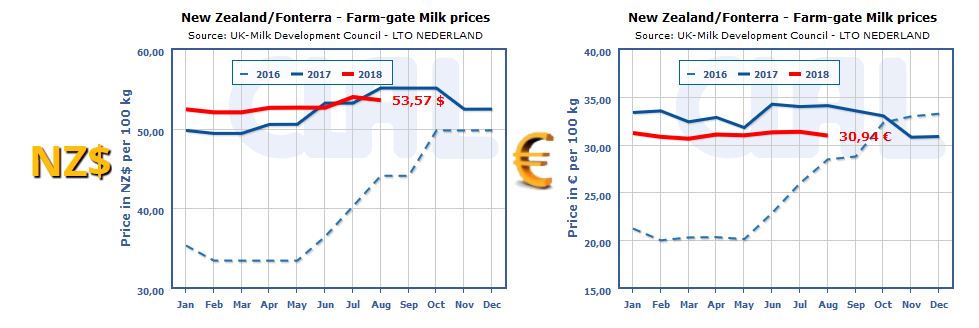

CLAL.it – Farmgate Milk Price in New Zealand (Fonterra)

– Assessments about market trend are expressed in US$;

– Dairy season: July, 1st – June, 30th (Australia), June, 1st – May, 31st (New Zealand);

– Source: USDA summarized by the CLAL Team

The CLAL.it team is composed of young people who with the help of Computer Science study the dairy market and develop tools to provide the Operators of the dairy sector with a comprehensive real-time view of the national and international market trends.