EU-28 Cheese Export: balance between U.S. and Japan?

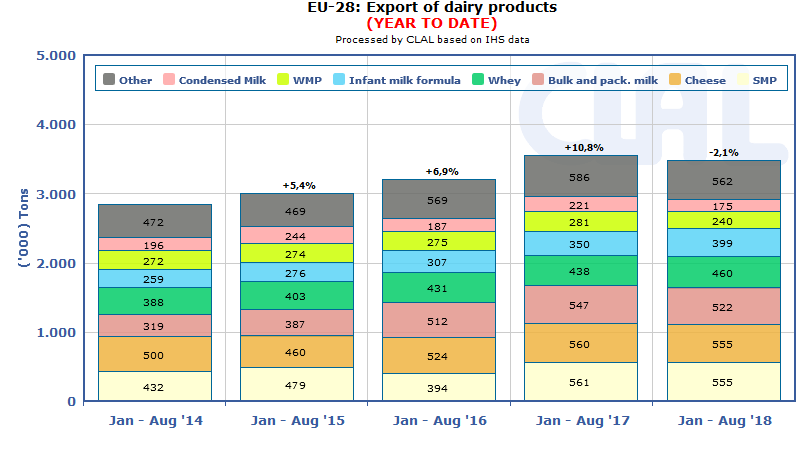

The dairy exports of the European Union are going through a period of uncertainty. Between January and August 2018, exports fall in quantity (-2.1%) and in value (-5.1%), compared to the first eight months of 2017.

Export in Milk Equivalent (ME) drops 3.8%, after the 2017 boom (+19.04%), with negative exports to Southeast Asia, Central and South America and, to a lesser extent, North America.

The world looks for products with high added value in the EU

If we analyze the trend of individual dairy products, it emerges that the world is looking for high added value and highly specialized products in Europe. In fact, the best performance of the EU-28 are for Infant milk formula (+14% in quantity and +4.8% in value), with China, Hong Kong and Saudi Arabia among the main importers, for Caseins (+24.4% in quantity and +0.7% in value), with the U.S. and Mexico the first buyers, and Lactose for pharmaceutical use (+4.4% in volumes), with China, New Zealand and Japan among the top importers.

EU Cheese Export

-7% to the U.S.

+13% to Japan

Jan-Aug 2018

EU exports less Cheese in January-August 2018: -0.8% in quantity and -1.2% in value. The United States, the first country of destination, lost -7% y-o-y in eight months. Japan partially compensates, growing by +13%.

Milk deliveries in the EU recorded +1.4% in the first 8 months of 2018. Deliveries in August 2018, a month of drought, are unchanged compared to August 2017.

The slowdown in exports, combined with an increase in EU deliveries, could influence supply and demand in the future, with effects also on EU-28 prices.

CLAL.it – EU-28 Dairy Export (Jan-Aug)

The CLAL.it team is composed of young people who with the help of Computer Science study the dairy market and develop tools to provide the Operators of the dairy sector with a comprehensive real-time view of the national and international market trends.