News Oceania n°8/2014

Period: March 31 – April 11, 2014; Source: USDA

MILK PRODUCTION

AUSTRALIAN milk production is trending seasonally lower. Producer margins remain good but are narrowing as feed costs are slightly increasing.

The response of the Australian dairy industry to the recent trade agreement between Australia and Japan wasn’t so positive because the tariff levels for fresh cheeses didn’t change.

Milk production in NEW ZEALAND remains very positive and the prolonged season has allowed dairy manufacturers to build adequate supplies to cover contract needs.

Producers are looking to expand herds and increase milk production

- New Zealand *: +5,71 % (Jun 13 – Jan 14 vs. Jun 12 – Jan 13)

- Australia *: -1,83 % (Jul 13 – Feb 14 vs. Jul 12 – Feb 13)

BUTTER (82%): prices have retracted as the largest export markets have reduced purchases; production is covering domestic contracts; AMF prices continue to decline and export interest has diminished.

CHEDDAR CHEESE: weak market; production near the seasonal low point and geared to covering contracts; limited spot market.

SMP: prices and demand decreases although export interest in Southeast Asia is still active; the increased demand from cream, ahead of the Easter holidays, has led to some increases in SMP production.

WMP: prices declined significantly as China has adequate supplies and decreased purchases; for a number of weeks to come, market will continue to experience downward pressure and decreased export activity.

Dairy product prices have weakened, due to global milk production increases and a decline in sales to China. The FAO Dairy Price Index averaged 268.5 points in March, a fall of 2.5 percent, over February.

Many Buyers are holding off purchases hoping in further declines in prices.

Note: · Assessments about market trend are expressed in US$;

· * Dairy season: July, 1st – June, 30th (Australia), June, 1st – May, 31st (New Zealand)

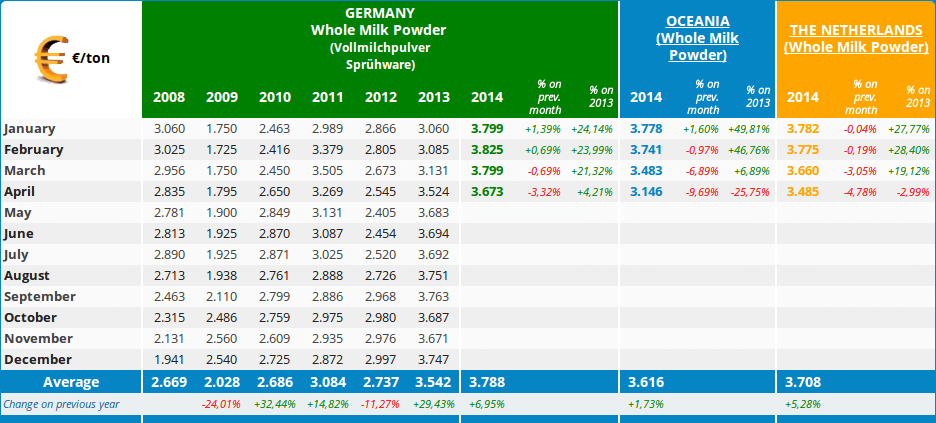

CLAL.it – Comparison among Whole Milk Powder (WMP) Prices in Germany, Oceania and the Netherlands

Degree in Economics with focus in Marketing and Sales, she belongs to the CLAL.it Team. The CLAL.it Team is composed of young people who, with the help of Computer Science, study the dairy market and develop tools to provide the Operators of the dairy sector with a comprehensive real-time view of the Italian and international market trends.

Leave a Reply

You must be registered and logged in to post a comment.