Dairy supply, demand and prices in Oceania and South America [The Austral – May 2021]

The Austral news concentrates the latest information on the dairy market in Oceania and South America.

Oceania: Fonterra has invested in a new foodservice application centre in China

Australian current milk production is near the seasonal low. Fonterra announced its opening milk price for Australia for the new season 2021/22: 6,55 AUD/kg MS. The price is 15 cents/kg MS higher than last year’s opening price.

- 30,86 €/100 kg of milk with 4.0% fat and 3.4% di protein weight/weight (ref. Germany)

(current exchange rate taken as reference: 1 AUD = 0,63629103 €).

Milk deliveries New Zealand+1.8%Jun20 – Mar21

As of 2024 dairy export to China will be duty-free

Fonterra has invested in a new food service application centre in Guangzhou where it tests dairy innovations with its Chinese customers. Dairy products with added value are highly appreciated by the Chinese market.

CLAL.it – New Zealand dairy export to China

New Zealand milk production is near the seasonal low, as the end of the season on May 31 moves closer, and upward dairy commodity price pressure is expected.

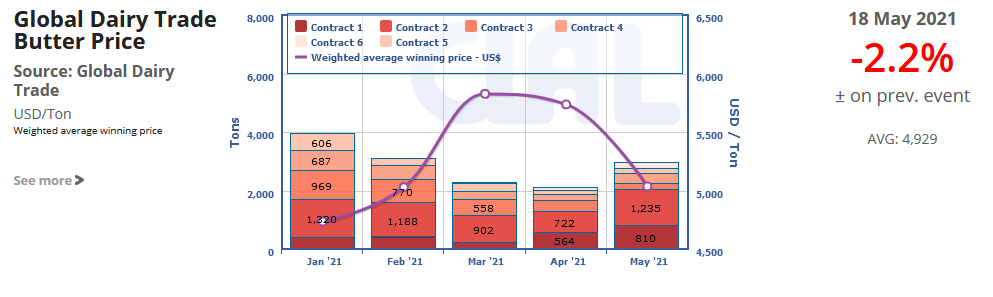

In the North Island areas of Waikato and Taranaki there is a greater concentration of Butter plants, and the increase in milk production in recent months in these areas is absorbed by a greater production of Butter. The addition of butter to GDT volumes resulted in weaker butter prices.

The price of Cheddar is also decreasing. Price quotes from the U.S. are often lower than from Oceania. This has imposed some downward pressure on Oceania Cheddar pricing.

SMP and WMP buying interest from China and countries in Southeast Asia has helped maintain firming prices.

The GDT event on May 18 recorded a slight decline in the average price (-0.2%), compared to the previous event. Positive changes for Cheddar (+1%) and SMP (+0.7%) and decreases for WMP (-0.2%) and Burro (-2.2%).

CLAL.it – Butter prices and offered volumes at GDT

South America: some pressure on margins for dairy operators

The data for the first quarter of 2021 relating to milk deliveries in South America show increases in Argentina (+4.8%), Brazil (+1.3%, provisional figure), Chile (+0.4%) and Uruguay ( +6.8%).

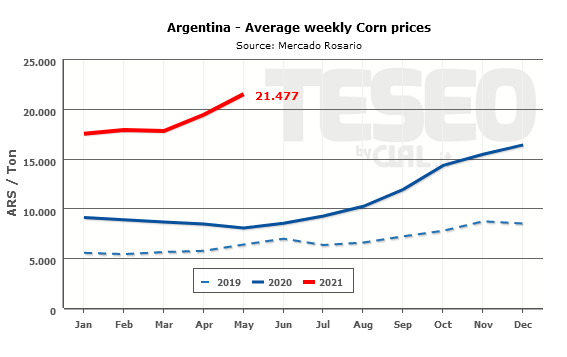

Brazilian milk producers are experiencing an unfavorable scenario, due to the sharp increase in production costs and reductions in the price of milk. However, the weekly trend in Corn and Soybean prices signals a slight decrease in progress.

Although some locations in Brazil have been hit by the rains, the water deficit situation remains, with a negative impact on soil moisture.

Corn and Soybean prices in Argentina are at historical highs

Milk Powders prices are decreasing. After a period of increased demand for immediate needs, the SMP trading activities have slowed in the Southern Cone (Chile, Argentina, Uruguay and Paraguay). There is also a slight decline in demand for WMP. Manufacturers’ inventory levels are limited.

TESEO.clal.it – Corn prices in Argentina

Source: CLAL processing on USDA, IHS and local sources.

Note: assessments about market trend are expressed in US$

The CLAL.it team is composed of young people who with the help of Computer Science study the dairy market and develop tools to provide the Operators of the dairy sector with a comprehensive real-time view of the national and international market trends.