Increasing EU demand for Corn [Corn and Soybean – n°9/2017]

Global Corn production for 2017-18 (season started on September 1st) is expected to be 1032.63 Mio t, slightly down (-0.1%) compared to August estimates. Expected increases in the United States, Argentina and Mexico are offset by lower production in the European Union and Ukraine.

The U.S. crop is estimated at 360.30 Mio t (+0.2%). Corn used for ethanol is projected down 25 million bushels, based on observed usage during 2016-17 and expectations of lower exports. With supply increasing and use falling, Corn ending stocks are +2.7% from last month. Global Corn stocks are lower from the last 3 seasons, with a significant reduction in China (-19.8%), the country with the highest share of stocks.

Export is projected higher for Ukraine (+2.3%), the fourth largest Corn exporter, after the U.S., Brazil and Argentina. Ukraine’s relatively large exportable supplies and logistical advantages are expected to fill demand for imported Corn in the EU.

Ukraine is the largest Italy’s Corn supplier: 1060.7 t in the first half of 2017.

Global Soybean production for 2017-18 (new season will start on October 1st) is projected at 348.44 Mio t, +0.3% from August estimates, mainly reflecting a larger crop in the U.S. (120.59 Mio t). With increased supplies and lower prices, U.S. Soybean exports are raised +1.1% leaving ending stocks unchanged.

In China, world’s largest Soybean importer, imports are expected to increase further: +1.06% from last month’s estimates, +3.26% from the previous season.

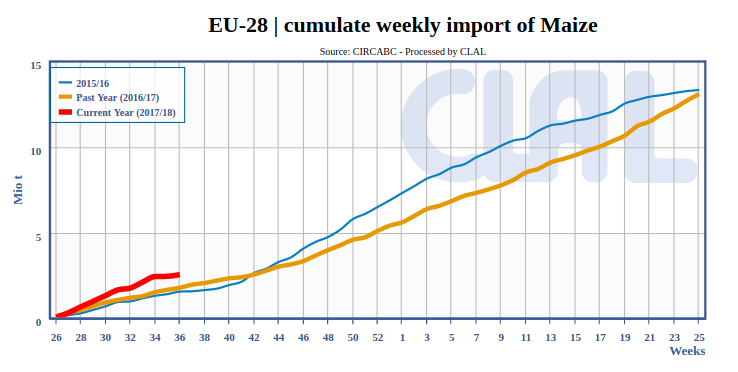

EU-28 | cumulate weekly import of Maize

-

-

MAIS-SOIA-EN-SET-2017.pdf (557 KB)

Corn & Soybeans - September 2017: Report about prices, production and global trade prospects for 2017-18 season.

Source: USDA

The CLAL.it team is composed of young people who with the help of Computer Science study the dairy market and develop tools to provide the Operators of the dairy sector with a comprehensive real-time view of the national and international market trends.

Leave a Reply

You must be registered and logged in to post a comment.